What does AI-generated document fraud look like in 2026?

Table of Contents

[ show ]- Loading table of contents...

Jessica Lara

My job is to look at documents that may not be what they claim to be.

Every day I review documents flagged across Inscribe's network: bank statements, pay stubs, invoices, tax forms. My work is pattern recognition at the document level. When I started at Inscribe, the patterns were mostly about templates: the same formatting artifacts appearing across dozens of submissions, the same layout quirks. You learn to recognize a template the way you learn to recognize a handwriting style.

In 2025, a new signal appeared. AI-generated documents. And the patterns changed.

I pulled our mid-year data in June 2026. Here is what I found.

How AI document fraud is growing

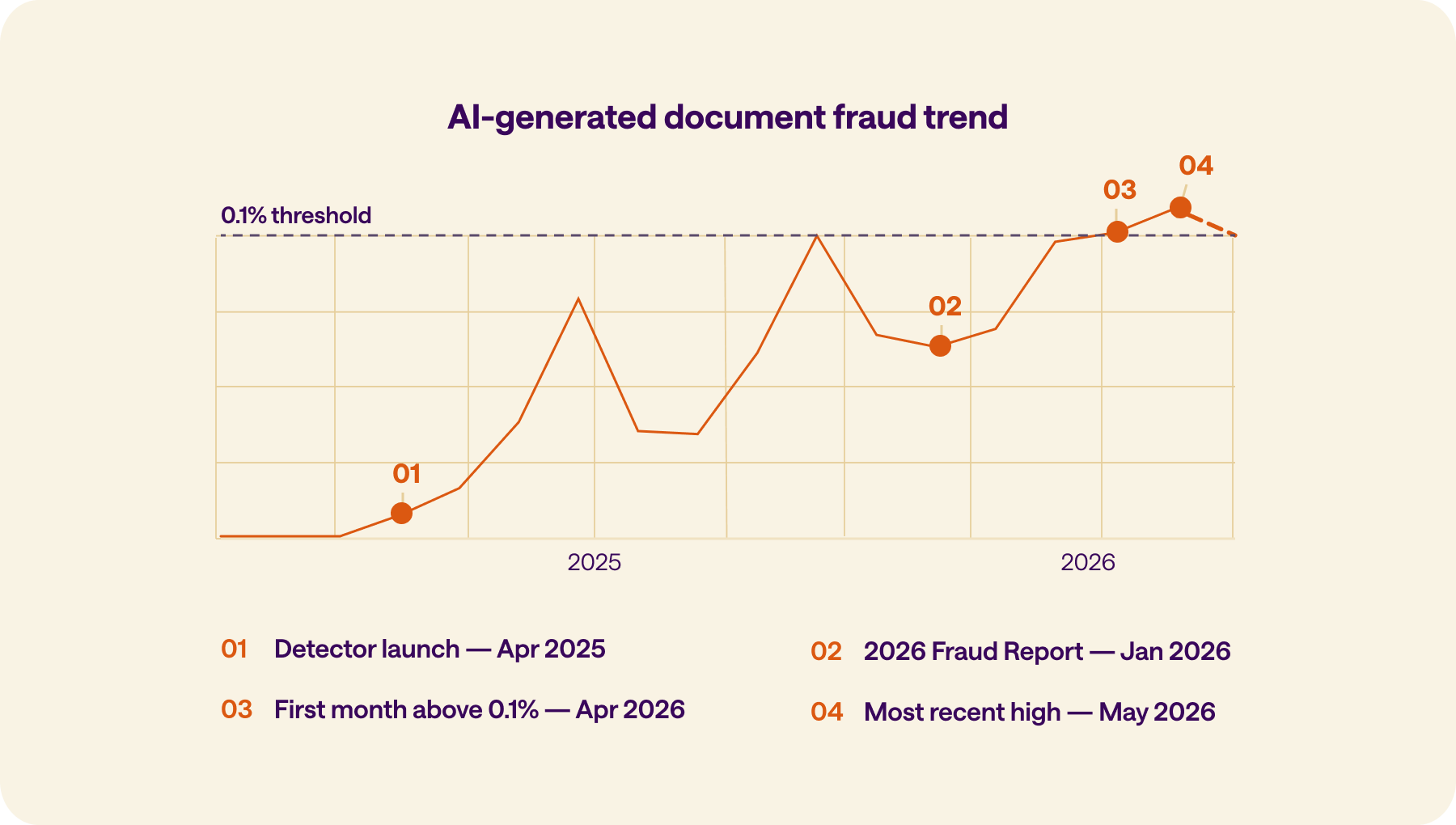

Since our AI_GENERATED detector launched in April 2025, the volume of AI-flagged documents across Inscribe's network has grown roughly 4x. The most recent months are the highest we have recorded. The chart below shows the full trajectory.

The shape of the curve matters as much as the volume. A spike is often a single fraud ring or a data artifact. This is a sustained climb, meaning the underlying behavior is spreading across more actors, more institutions, more document types.

What types of AI document fraud we see at Inscribe

Bank statements account for roughly one in four documents we flag as AI-generated. Invoices and payslips follow at similar rates. Together these three document types account for more than half of all AI-generated flags across our network.

That concentration makes sense when you consider what these documents unlock. A convincing fake bank statement opens the door to high-value credit approvals, business financing, mortgage decisions. Fraudsters target the documents that matter most to underwriters, because those are the ones worth faking.

A year ago, I could tell within seconds. The formatting was Excel-like: perfect table alignment, rounded transaction amounts, payees labeled "grocery store" instead of an actual merchant name. Real bank statements are messier. Real transactions say "Walmart" and "Shell" and have amounts like $47.13.

The documents I'm reviewing now require real scrutiny. Some require a second review, a cross-check against institutional patterns, or a direct conversation with a customer. The AI tooling used to generate them has improved significantly over the past 18 months.

Not all AI documents are made by LLMs

There are two categories of AI document fraud. We can detect both.

- The first: documents generated entirely by AI. Built from scratch using a tool, a template prompt, or a purpose-built fraud service. This is what this data reflects.

- The second: real documents with AI-altered fields. A genuine bank statement with the balance changed. A real pay stub with inflated income. The document structure is correct because it started from a real document. The alterations are targeted and precise.

The documents that concern me most are the legitimate ones altered using AI. Everything looks correct and expected, because most of it is. In my experience, this category is consistently harder to catch.

What’s changed since January?

The 2026 State of Document Fraud Report captured data through January. A few things have shifted since publication.

The growth has continued. The months since January have tracked higher than the same months a year prior. The trend hasn't flattened.

A new pattern has emerged. In June 2026, one of our lending customers flagged bank statements that appeared to have been generated by a bank's own AI tooling, documents that look legitimate because the infrastructure that produced them is real, just not associated with real accounts. This is different from typical fraudster-built fakes. Whether it represents a new fraud vector or an isolated case, we are actively investigating.

Template fraud is still here. AI-generated fraud gets the attention, but template-based fraud still runs at a rate 2 to 3x higher, consistently. I watch both signals every day. Sophisticated actors use both vectors, often in the same fraud wave. The full picture requires tracking the full spectrum.

What’s next for AI document fraud?

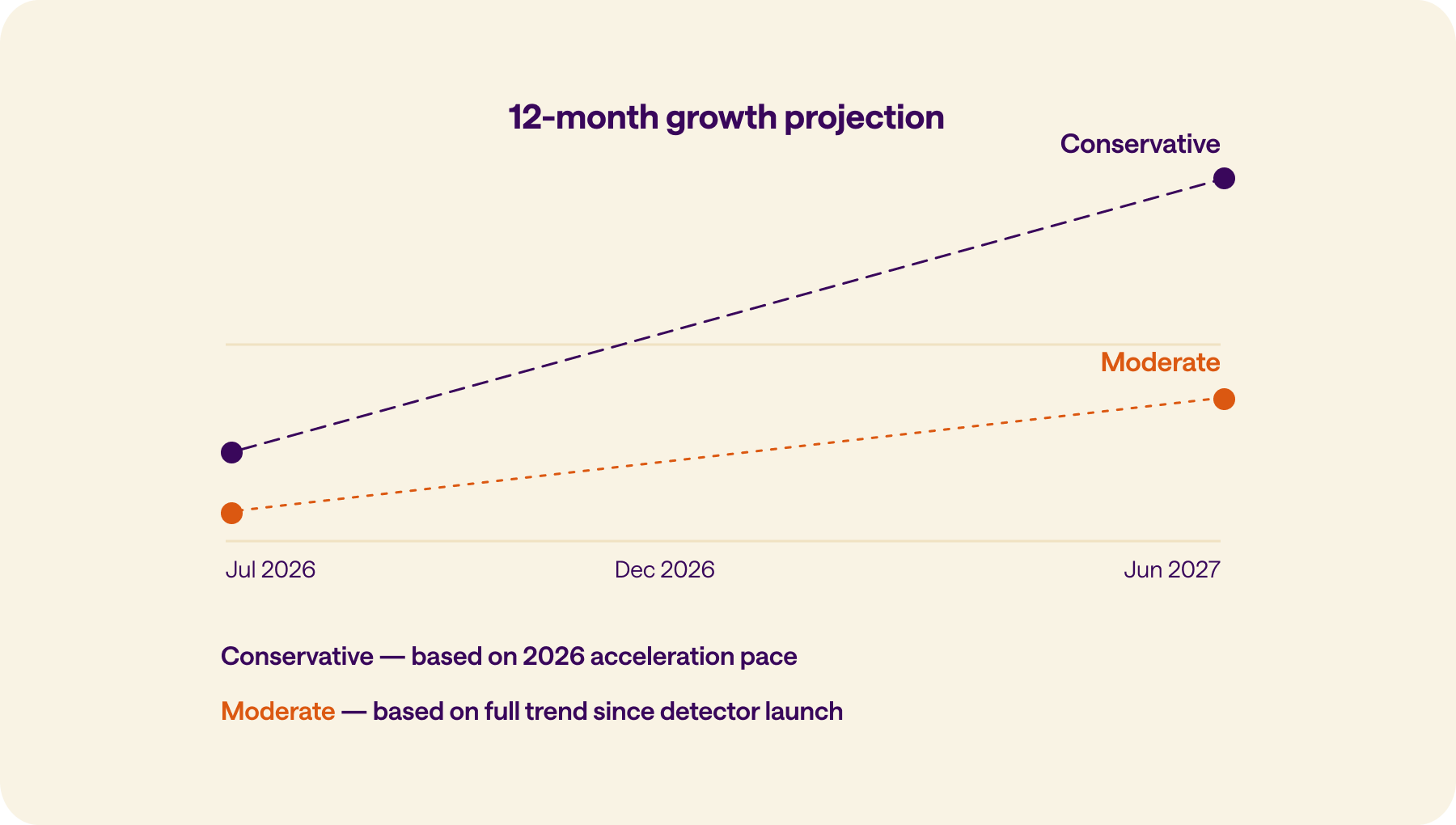

If current 2026 trends continue, AI-generated document fraud will track higher through the rest of the year and into 2027. The projection chart below shows two scenarios. Conservative and moderate lines point the same direction; the pace differs, but the trend does not.

What I watch more than the volume is the capability curve. Open-source models and purpose-built tools like FraudGPT operate without guardrails. The same improvements making commercial AI better at generating realistic documents are making their open-source counterparts better too. The barrier to using these tools is near zero.

On the detection side, the work is getting better. Cross-institution intelligence helps. Pattern matching across submissions and institutions helps. Every detector update that forces fraudsters to change their approach is evidence the system is working.

The advice I would give any fraud team: do not wait to see an AI flag in your own queue before taking this seriously. The barrier to submitting a fraudulent document is at an all-time low. The customer who committed fraud today may look identical to the customer you have trusted for years.

Both scenarios point the same direction: continued growth, with AI-generated fraud likely reaching a volume range comparable to template fraud by end of 2026 under the conservative model.

Emerging patterns not in the January report

The AI-edited gap

The more dangerous vector is AI-edited documents, which are real documents with AI-altered fields. Currently unmeasured in aggregate. "The more troubling documents I tend to come across are not the ones that have been generated using AI from scratch, but the legitimate documents that fraudsters use AI to alter." said another lending customer of ours.

Open-source models and FraudGPT

Major AI providers have implemented guardrails against generating fraudulent documents. Open-source alternatives and purpose-built tools like FraudGPT bypass these entirely. As closed-source guardrails improve, open-source becomes the tool of choice for sophisticated actors.

Every document I review tells part of a larger story. Looking at a single submission, it's easy to think AI-generated fraud is still rare or that today's techniques are good enough. But when you step back and look across millions of documents, the direction is clear. The tools are improving, the volume is growing, and the gap between real and fake continues to shrink. That's why our job isn't just to catch today's fraud. It's to anticipate where fraudsters are going next and build the detectors they'll run into before they get there.

Download the full 2026 State of Document Fraud Report today, or request a demo to see what our AI will find in your documents.

About the author

Jessica Lara is a Risk Operations Analyst at Inscribe, where she reviews documents flagged for potential fraud across Inscribe's network of U.S. financial institutions. She evaluates AI-generated and AI-edited documents daily, tracking how fraud patterns evolve across document types and submission methods.

What will our AI Agents find in your documents?

Start your free trial to catch more fraud, faster.